If you are a lender, technical, representative or most importantly a customer in BFSI Section, I would take it for provided you need to have heard the brand-new neologism "Digital Financial". In my circle, I did chat with a number of individuals and also interestingly, no 2 persons seem to regard this in very same way - well, this is type of overestimation, however you get the picture! This made me take a time out and believe what this could indicate to a person like me that is an insider in the market, to answer if a associate, pal, or someone at my box asks me concerning this. As a true CrossFit athlete I follow at least the first rule - tell every person you stumble upon concerning CrossFit.

The reason I raise CrossFit is not even if of my attraction or, also obsession. CrossFit is a little complicated and also intimidating to those inexperienced, however to place it just it is toughness and conditioning program, which enhances physical fitness. CrossFit defines health and fitness itself in regards to 10 components - Cardiovascular Stamina, Stamina, Versatility, Toughness, Power, Rate, Agility, Sychronisation, Precision, Equilibrium. But, usually if you ask any one of your good friends what is health and fitness, you could obtain multiple reactions. E.g. a runner will certainly state capacity to run half-marathon, or a weight lifter could claim deadlift of a minimum of 1.5 x body weight, or a man into yoga exercise may claim doing 108 Suryanamaskaras. Well, each of them may be right in their very own way. Your definition of health and fitness might be doing all of those, or you could simply claim I am fit enough if I have the ability to do my 9-to-5 task without taking any authorized leave in an assessment cycle.

On the same lines, financial institutions can translate Digital Financial in their very own terms and also likewise, people like you as well as me will certainly have formed some opinion based upon our very own direct exposure.

For many years, financial institutions of all shapes and sizes enhanced a great deal by adjusting to IT/ ITES (IT Enabled Services) and also they have actually accomplished diverse degrees of success. However, due to absence of focused as well as long term approach, production of disjointed systems, rapidly altering organisation and running circumstances, etc., the desired objectives may not have actually been fully recognized. Several of those " fell short" efforts might have been driven by the organization's urge to be an early adaptor of a innovation or pattern (betting on a wrong steed). On the contrary, we might lose a huge possibility, if we don't identify as well as bet on a winning equine. So, the trick is banking on the best equine, at a right time - i.e., when the odds are low. Commonly, industries utilize what is called a Buzz Cycle to review a new innovation or trend. If you are interested to understand what is a "hype cycle", please see Gartner's technique. I will certainly try to string with each other a few of the crucial elements of Digital Financial, as unlike a lot of the buzzwords, it is neither a solitary solution nor a technology.

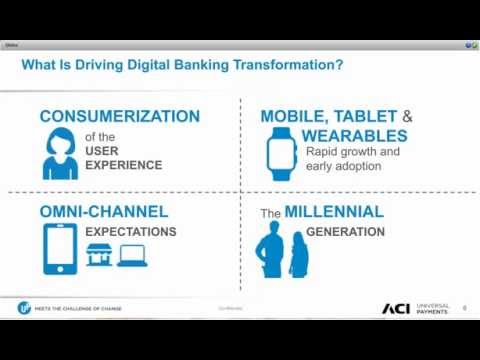

Just around the moment (2008-10) I spent about a year plus in Brussels, 3 large banks (Fortis, Dexia and also KBC) which always came across as incredibly danger averse bankers from the BeNeLux area, started facing significant stress and also their worth eroded dramatically and also triggered warmed discussions in the community - that assumed their money is always secure with the financial institutions (either as a depositor or share holder). What truly happened there, is really intricate. Trick elements being, huge sovereign debt floating in between 84 to 99% of GDP, absence of Government for 533 days, etc. These activated liquidity problems. If you include in this various other upheavals in the financial market around the world, it is easy to understand that the " trust fund" within the system was under threat. Exactly how would certainly we develop trust? By being transparent. Consumers require (not desire!) openness in the entire system. Younger the customer base, that require felt is more intense. This, when you look from the altering client experience and also expectations from retail industry (Amazon, Flipkart), transport (Uber, Ola), food market (Zomato, FoodPanda, ZaptheQ), you understand where the financial industry is. Clients have reset the expectations in regards to value, experience, and choices. The Secret takeaway for the lender - Individual Experience - abundant, uniform, mobile (anywhere), safe and secure, enhanced worth.

Many individuals I have engaged with just recently on this topic, suggested Internet Banking or Mobile Financial as Digital. Yes, this is only the beginning of what could be Digital Financial. Possibly, they cover earlier collection of consumer assumptions. Going on, could we see a day soon, where there is no paper in any one of the financial transactions? When I state paper, I am not simply describing currency! Couple of points which are already in practice in few financial institutions and getting energy throughout are - digitizing procedures within the bank (like customer on-boarding, loan application), cheque truncation systems which allows you to take a photo of the cheque on your mobile and also send out to your financial institution, and so on - there by bringing performance in decisionmaking, capability to customize procedures to certain client demands, conserve some unnecessary trips to the branch, and so on. This could suggest simply put, implementing paper/ image management systems, service process management and also monitoring systems, incorporating these components within the existing IT solutions. The Trick - digitizing interior processes.

Social media site in the last few years have actually brought greatest effect across borders - be it, Tahrir Square change, Ice Bucket Difficulty, which mobile to buy, just how we order and also pay for lunch or determining a https://www.sandstone.com.au/en-au/cloud fine eating area as well as going Dutch while sharing the expense. Social media site is already bring interruptions in regards to which financial institution to trust, what they can anticipate from a bank in terms of services, offer a voice to their dissatisfaction. Which subsequently indicates, banks have to be on the exact same Social media site paying attention to their consumers, selling their solutions as well as likewise ultimately, drawing in brand-new customers, keeping the customers as well as more notably, coming to be "The Goto Financial institution" if the client has numerous accounts. As an example, what could not have been anticipated couple of years back, in Kenya, among our prestigious client's Twitter handle (@ChaseBankKenya) makes use of Twitter to connect, launch as well as share CSR activities, as well as address consumers' inquiries and also problems extremely successfully. That is, The Reach element.

One more quiet point taking place behind the walls in a bank is called Information Analytics or Big Data. These churn out unprecedented understandings into client habits and preferences, driving incredibly concentrated techniques. These also assist customers to understand their invest analysis, intend their spending plans, economic objective administration and so on

. In addition to these essential parts, there are a number of others which can make the financial institution much more " electronic" - chat and also video clip discussion facilities to bring financial institution closer to the customer when he/she requires it, or enlightening customers through online tutorials like economic proficiency, tax planning, etc., integrating numerous options and systems in the bank to reduce information replication and redundancy and also aiding the financial institution make even more Straight With Handling systems there by lowering errors, price of operations, and also boosting efficiency in the whole system. Banks can significantly boost seamless data exchange with others partners like regulative bodies, clients, federal government bodies thus making entire procedure far more clear and reliable.

Ultimately, the large inquiry is what should be achieved from the big task checklist to call a financial institution "Digital Financial institution"? Just like in health and fitness, there is no solitary remedy or the best option. Each bank needs to define its own strategy, execution plan to reach the goal of client joy, operation performance, as well as total share holders' improved worth.

With our sharp concentrate on Core Financial Solutions, as well as wide range of experiences in consulting, execution, testing, incorporating several solutions at numerous banks across the globe, we at SandStone will certainly be glad to engage with you or your group to aid understand a few of these goals.